European Food Processing Automation Market Size & Forecast 2026–2034

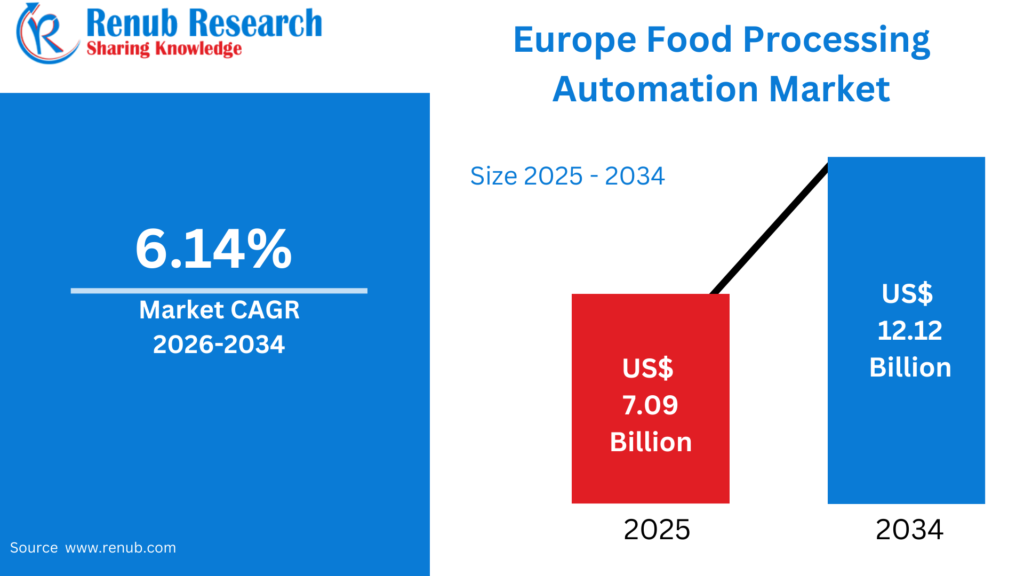

According to Renub Research European food processing automation market is expected to witness steady and resilient growth over the forecast period, supported by structural changes in food consumption, labor dynamics, and regulatory frameworks. The market is projected to expand from US$ 7.09 billion in 2025 to US$ 12.12 billion by 2034, registering a compound annual growth rate (CAGR) of 6.14% between 2026 and 2034. Automation has become a strategic necessity for food manufacturers across Europe as they strive to improve productivity, ensure food safety compliance, reduce operational costs, and respond to growing demand for processed and convenience foods.

Europe’s food industry is one of the most regulated and technologically advanced in the world. Rising labor shortages, increasing wage pressures, and stricter hygiene and traceability standards are accelerating investments in automation technologies such as industrial robotics, distributed control systems, sensors, and advanced software platforms. As Industry 4.0 principles gain wider acceptance, food processing automation is becoming a core pillar of competitiveness and sustainability across the European food value chain.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=europe-food-processing-automation-market-p.php

European Food Processing Automation Market Outlook

Food processing automation refers to the application of automated equipment, control systems, and digital software across food manufacturing processes such as sorting, grading, slicing, mixing, heating, cooling, and packaging. These systems enable food processors to achieve consistent product quality, higher throughput, reduced waste, and improved operational efficiency. Automation technologies include conveyor systems, industrial robots, programmable logic controllers, distributed control systems, and manufacturing execution systems.

In Europe, food processing automation has gained strong momentum due to increasing demand for packaged and processed foods, rising regulatory scrutiny, and escalating labor costs. Food manufacturers are under constant pressure to deliver safe, standardized, and traceable products while maintaining profitability. Automation addresses these challenges by minimizing human intervention, reducing contamination risks, and ensuring process repeatability. Additionally, sustainability objectives such as energy optimization, reduced food waste, and efficient resource utilization further support automation adoption across the region.

Increasing Demand for Processed and Convenience Foods

The growing consumption of processed, packaged, and ready-to-eat foods is a major driver of food processing automation in Europe. Urbanization, changing lifestyles, and an expanding working population have increased demand for convenient food options with extended shelf life and consistent quality. Consumers increasingly prefer frozen meals, bakery products, dairy items, beverages, and ready meals that require minimal preparation time.

Food producers are therefore under pressure to scale production while maintaining uniform taste, texture, and safety standards. Automation enables high-speed, continuous production and supports diverse packaging formats across multiple product categories. Automated systems also allow manufacturers to quickly adapt to changing consumer preferences and product variations. As demand for convenience foods continues to rise across Europe, automation will remain essential for meeting volume, quality, and efficiency requirements.

Stringent Food Safety and Hygiene Regulations

Strict food safety and hygiene regulations in Europe play a critical role in driving the adoption of food processing automation. European food safety frameworks emphasize traceability, contamination prevention, and standardized quality control throughout the production process. Automation significantly reduces direct human contact with food products, thereby minimizing contamination risks and ensuring compliance with hygiene standards.

Automated systems enable precise monitoring, documentation, and control of processing conditions, which is essential for regulatory audits and recalls. Centralized control platforms improve transparency across production stages, from raw material handling to final packaging. As regulatory expectations continue to evolve and enforcement becomes more stringent, automation investments are increasingly viewed as a necessity rather than an option for European food processors.

Labor Shortages and Rising Operating Costs

Labor shortages across the European Union are accelerating the adoption of food processing automation. The food processing industry relies heavily on repetitive, physically demanding tasks that often experience high turnover rates. At the same time, rising wages and difficulty in attracting skilled workers are increasing operational costs for food manufacturers.

Automation provides a long-term solution by reducing dependency on manual labor and enabling 24/7 operations without proportional increases in labor expenses. Although automation requires high upfront capital investment, the long-term benefits in productivity, cost control, and workforce stability make it highly attractive. In regions facing acute labor shortages, automation has become essential for sustaining production capacity and competitiveness.

Europe Food Processing Distributed Control Systems Market

Distributed control systems (DCS) play a vital role in Europe’s food processing automation landscape by enabling centralized monitoring and precise control of complex production processes. DCS platforms integrate multiple processing stages, including raw material handling, cooking, fermentation, and packaging, into a single control environment.

These systems improve process stability, reduce downtime, and enhance traceability, which is critical for regulatory compliance. European food processors increasingly deploy DCS solutions to optimize energy usage, improve production reliability, and ensure consistent product quality. Large-scale applications are particularly prominent in dairy processing, beverage manufacturing, and ready-meal production, where continuous operations demand high levels of automation.

Europe Food Processing Automation Hardware Market

The automation hardware segment forms the backbone of Europe’s food processing automation market. It includes processing machinery, industrial robots, sensors, actuators, controllers, motors, and conveyor systems used across production lines. Demand for durable, food-grade hardware capable of operating under harsh processing conditions continues to rise.

European manufacturers emphasize hygienic design, corrosion resistance, and ease of maintenance in automation hardware. Recent technological advancements include smart sensors, collaborative robots, and vision systems that improve accuracy, flexibility, and safety. As food processors modernize existing facilities and invest in new production lines, demand for advanced automation hardware is expected to remain strong.

Europe Dairy Processing Automation Market

The dairy sector is one of the most automated segments within Europe’s food processing industry. Automation is widely used in milk collection, pasteurization, fermentation, filling, and packaging processes to ensure cleanliness, precision, and high throughput. Dairy products are particularly sensitive to contamination, making automation essential for meeting stringent hygiene requirements.

Rising consumption of value-added dairy products such as cheese, yogurt, and functional beverages is driving demand for advanced automation solutions. Automated systems enhance product consistency, reduce waste, and improve energy efficiency. Due to strict regulatory oversight and high quality expectations, the dairy sector continues to lead in automation adoption across Europe.

Europe Food Processing Packaging and Re-packaging Market

Packaging and re-packaging automation is a major growth area within the European food processing automation market. Automated packaging systems handle filling, sealing, labeling, sorting, and palletizing with minimal human intervention. These systems enable high-speed processing while maintaining accuracy and compliance with labeling regulations.

Re-packaging automation has gained traction due to the growth of private labels, portion-controlled packaging, and promotional variants. Automation allows manufacturers to respond quickly to changing consumer demands and sustainability requirements. As packaged and ready-to-eat food consumption increases, investment in automated packaging and re-packaging solutions is expected to accelerate.

Europe Fully-Automatic Food Processing Automation Market

Fully automatic food processing systems are increasingly adopted by large food manufacturers seeking maximum efficiency, scalability, and consistency. These systems manage entire production lines with minimal human involvement, significantly reducing labor costs and human error. Fully automated lines ensure continuous processing, high throughput, and strict hygiene compliance.

Although capital investment requirements are high, the long-term benefits of reduced operational costs, improved productivity, and standardized output make fully automatic systems highly attractive. Persistent labor shortages and growing demand for standardized food products continue to drive adoption of fully automatic food processing automation across Europe.

Europe Semi-Automatic Food Processing Automation Market

Semi-automatic automation solutions cater primarily to small and medium-sized food processors seeking a balance between efficiency and investment cost. These systems combine automated machinery with human oversight, offering flexibility and control while improving productivity.

Semi-automatic solutions are commonly used for specialty foods, artisanal products, and regional manufacturing operations. They allow gradual upgrades without complete system replacement, making them appealing to processors with budget constraints. The ability to support customization and niche production strategies ensures continued relevance of semi-automatic automation in the European food industry.

French Food Processing Automation Market

France’s food processing automation market is driven by the country’s strong emphasis on food quality, purity, and traceability. Automation adoption is growing across dairy, bakery, meat, and beverage sectors to ensure consistent quality and regulatory compliance. French manufacturers are upgrading processing lines to improve efficiency while maintaining traditional product standards.

Robotic handling, automated packaging, and inspection systems are increasingly deployed to reduce costs and improve hygiene. Sustainability goals, including energy efficiency and waste reduction, further support automation investments. Small and medium-sized processors are gradually adopting scalable automation solutions to remain competitive.

Germany Food Processing Automation Market

Germany represents one of the most advanced food processing automation markets in Europe, supported by strong engineering capabilities and early adoption of Industry 4.0 principles. German food processors emphasize precision, efficiency, and compliance with strict food safety regulations.

Automation is widely used in meat processing, confectionery, beverages, and ready-to-eat foods. Digital monitoring, predictive maintenance, and smart factory solutions enhance productivity and reduce downtime. Labor shortages and rising operational costs continue to reinforce demand for advanced automation technologies across Germany’s food industry.

United Kingdom Food Processing Automation Market

The UK food processing automation market is driven by the need to improve efficiency and address workforce shortages. Automation is increasingly adopted in packaging, sorting, inspection, and handling processes within bakery, meat, and ready-meal segments.

Food processors rely on automation to ensure compliance with food safety and traceability standards while controlling costs. Rising demand for convenience foods and private-label products is driving the need for flexible and versatile automation solutions. The UK market continues to transition toward higher levels of automation to maintain production stability.

Russia Food Processing Automation Market

Russia’s food processing automation market is expanding gradually as domestic food production increases. Automation adoption is growing across dairy, meat, and grain processing sectors to improve efficiency and product consistency. While adoption remains uneven, particularly among small processors, long-term productivity needs are driving steady investment in automation solutions.

As food manufacturers seek to modernize facilities and reduce operational inefficiencies, automation is expected to play a growing role in Russia’s food processing industry over the coming years.

Market Segmentation Overview

The European food processing automation market is segmented by operational technology and software, component, end-user, application, automation level, and country. Key technologies include distributed control systems, manufacturing execution systems, industrial robotics, sensors, motors, and control devices. End-user industries span dairy, bakery and confectionery, meat and seafood, fruit and vegetable processing, and beverage manufacturing. Automation levels range from fully automatic to semi-automatic lines across major European countries.

Competitive Landscape and Company Analysis

The European food processing automation market is highly competitive and innovation-driven, with global and regional players focusing on digitalization, robotics, and smart factory solutions. Companies are evaluated across overviews, key leadership, recent developments, SWOT analysis, and revenue performance. Major participants in this market include ABB Ltd., Alfa Laval AB, Baader Food Processing Machinery GmbH, Bosch Rexroth AG, Bühler Holding AG, Endress+Hauser Group Services AG, Emerson Electric Co., FANUC Corp., Festo SE & Co. KG, and GEA Group AG. These players continue to shape the European food processing automation market through technological innovation, strategic partnerships, and expansion of integrated automation solutions.