Japan Ultrasound Device Market Size and Forecast 2025–2033

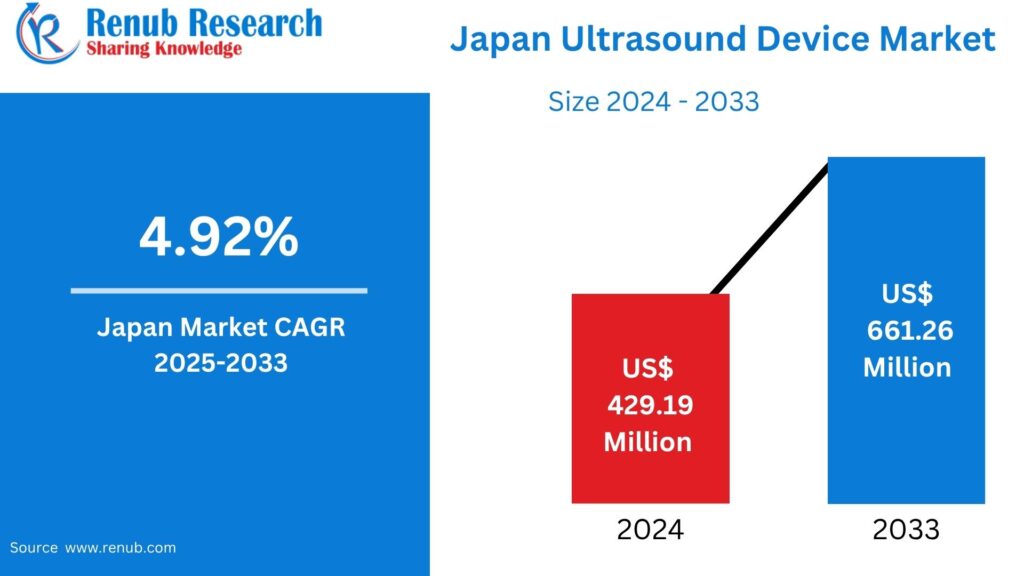

According To Renub Research Japan ultrasound device market is projected to experience steady and sustained growth over the forecast period from 2025 to 2033. The market is expected to expand from a valuation of US$ 429.19 million in 2024 to approximately US$ 661.26 million by 2033, registering a compound annual growth rate of 4.92%. This growth reflects the increasing reliance on ultrasound technology as a frontline diagnostic and therapeutic imaging solution across Japan’s healthcare system. Rising healthcare demand, technological innovation, demographic changes, and a growing emphasis on minimally invasive procedures are collectively shaping the trajectory of this market.

Japan Ultrasound Device Market Overview

Ultrasound devices are medical imaging instruments that use high-frequency sound waves to generate real-time images of internal body structures. These systems are widely used because they are non-invasive, safe, and do not involve ionizing radiation. In Japan, ultrasound technology plays a critical role in diagnosing and monitoring conditions affecting organs such as the liver, kidneys, pancreas, gallbladder, uterus, ovaries, prostate, thyroid, and vascular system. It is also indispensable in obstetrics for monitoring fetal development throughout pregnancy.

Beyond diagnostic imaging, ultrasound devices support interventional procedures by enabling accurate needle guidance for biopsies, tumor ablation, and fluid drainage. They are also increasingly applied in musculoskeletal assessments, cardiovascular evaluations, and metabolic bone disorder analysis. The versatility and safety profile of ultrasound make it one of the most frequently used imaging modalities in Japanese healthcare settings, ranging from large hospitals to outpatient clinics and specialized diagnostic centers.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=japan-ultrasound-devices-market-p.php

Role of Ultrasound in Japan’s Disease Burden

Japan faces a significant burden of chronic and age-related diseases, which directly influences the demand for ultrasound devices. Cardiovascular diseases, including cerebrovascular disorders, coronary artery disease, and carotid artery disease, are among the leading causes of morbidity. Ultrasound imaging is routinely used to assess blood flow, detect arterial blockages, and monitor heart structure and function.

Musculoskeletal disorders also represent a major public health concern, particularly among the elderly population. Chronic pain conditions affecting joints, muscles, and connective tissues often require ultrasound for diagnosis and treatment monitoring. Additionally, the rising incidence of metabolic and endocrine disorders has increased the use of ultrasound for thyroid and abdominal examinations. These factors collectively reinforce ultrasound as an essential diagnostic tool within Japan’s healthcare ecosystem.

Impact of Aging Population on Market Growth

One of the most influential drivers of the Japan ultrasound device market is the country’s rapidly aging population. Japan has one of the highest proportions of elderly individuals globally, with nearly one-third of its population aged 65 years or older. Aging is strongly associated with an increased prevalence of chronic illnesses such as cardiovascular disease, cancer, osteoporosis, and degenerative musculoskeletal conditions.

Elderly patients often require frequent diagnostic imaging for early detection, disease progression monitoring, and treatment planning. Ultrasound is particularly well suited for this demographic due to its safety, repeatability, and cost-effectiveness. As demand for long-term care, routine health screenings, and chronic disease management continues to rise, healthcare providers are increasingly investing in ultrasound systems to meet the needs of an aging society.

Technological Advancements in Ultrasound Devices

Technological innovation is transforming the ultrasound device market in Japan. Modern ultrasound systems now incorporate advanced imaging features such as three-dimensional and four-dimensional visualization, significantly improving diagnostic accuracy and clinical confidence. These capabilities are especially valuable in cardiology, obstetrics, and gynecology, where detailed anatomical and functional insights are critical.

Artificial intelligence and machine learning are also being integrated into ultrasound platforms to enhance image interpretation, automate measurements, and assist in anomaly detection. These technologies help reduce operator dependency and improve workflow efficiency, enabling faster and more accurate diagnoses. Advances in transducer design, signal processing, and software optimization have further improved image resolution and penetration, making ultrasound applicable to a wider range of clinical scenarios.

Growth of Portable and Handheld Ultrasound Devices

The increasing adoption of portable and handheld ultrasound devices is reshaping diagnostic practices in Japan. Compact ultrasound systems offer significant advantages in terms of mobility, ease of use, and affordability. They are particularly valuable in emergency departments, ambulatory care centers, rural clinics, and home healthcare settings.

Point-of-care ultrasound enables clinicians to perform immediate assessments at the patient’s bedside, reducing diagnostic delays and improving clinical decision-making. In Japan, where healthcare accessibility for elderly and rural populations is a growing concern, portable ultrasound devices support decentralized care delivery models. Their expanding use beyond traditional hospital environments is contributing substantially to overall market growth.

Increasing Demand for Minimally Invasive Procedures

Minimally invasive medical procedures are gaining popularity in Japan due to their benefits, including reduced recovery time, lower complication rates, and shorter hospital stays. Ultrasound plays a vital role in guiding minimally invasive interventions such as biopsies, catheter placements, pain management injections, and tumor ablation therapies.

As clinicians increasingly prefer image-guided procedures over conventional surgical approaches, the demand for high-quality ultrasound imaging continues to rise. This trend is particularly evident in oncology, orthopedics, and pain management, where precision and real-time visualization are essential. The growing preference for minimally invasive care is therefore a significant contributor to the expansion of the ultrasound device market.

Challenges Related to High Equipment Costs

Despite its many advantages, the adoption of advanced ultrasound equipment in Japan faces challenges related to high costs. Premium systems equipped with advanced imaging features, artificial intelligence, and sophisticated software require substantial capital investment. In addition to purchase costs, expenses associated with installation, training, and maintenance can be considerable.

These financial barriers are especially challenging for small clinics, outpatient facilities, and healthcare providers in rural or underserved regions. Limited budgets may force such institutions to rely on older or less advanced equipment, slowing the widespread adoption of next-generation ultrasound technologies. Addressing affordability concerns remains a key challenge for market participants seeking broader penetration.

Market Saturation in Urban Healthcare Centers

Japan’s major urban centers, including Tokyo and Osaka, have highly developed healthcare infrastructures with widespread access to advanced medical imaging technologies. Most large hospitals and specialty clinics in these regions are already well equipped with modern ultrasound systems, resulting in market saturation.

This saturation limits opportunities for new entrants and constrains growth for established manufacturers within metropolitan areas. Consequently, companies are increasingly targeting rural and semi-urban markets for expansion. However, these regions often face lower patient volumes, limited funding, and infrastructure constraints, requiring tailored strategies to stimulate demand and ensure sustainable market growth.

Product Segmentation of the Market

The Japan ultrasound device market is segmented by product into diagnostic ultrasound systems and therapeutic ultrasound systems. Diagnostic ultrasound systems dominate the market due to their extensive use across multiple medical specialties. Therapeutic ultrasound systems, while representing a smaller share, are gaining traction in applications such as physiotherapy, pain management, and targeted tissue treatment.

Each product category addresses distinct clinical needs, and ongoing innovation continues to expand their scope of application. Manufacturers are focusing on enhancing functionality, improving user interfaces, and integrating advanced technologies to differentiate their offerings within these segments.

Segmentation by Portability and Display Type

Based on portability, the market is divided into trolley or cart-based ultrasound devices and compact or handheld ultrasound devices. Cart-based systems remain widely used in hospitals due to their robust performance and advanced imaging capabilities. However, compact and handheld devices are witnessing faster growth due to their flexibility and suitability for point-of-care use.

In terms of display type, the market includes color ultrasound devices and black-and-white ultrasound devices. Color ultrasound systems are more commonly used as they provide enhanced visualization of blood flow and tissue characteristics. Black-and-white systems continue to be used in basic diagnostic applications and cost-sensitive settings.

Application and End User Segmentation

Ultrasound devices in Japan are utilized across a broad range of applications, including radiology and general imaging, cardiology, gynecology, vascular imaging, urology, and other specialized fields. Radiology and cardiology represent major application areas due to high patient volumes and frequent diagnostic requirements.

End users of ultrasound devices include hospitals, surgical centers, diagnostic centers, maternity centers, ambulatory care centers, and academic institutions. Hospitals account for the largest share of demand, driven by comprehensive diagnostic services and high patient throughput. Ambulatory and diagnostic centers are emerging as important growth segments due to the shift toward outpatient care.

Competitive Landscape and Company Analysis

The competitive landscape of the Japan ultrasound device market is characterized by the presence of established global and domestic manufacturers. Key players focus on product innovation, strategic collaborations, and portfolio expansion to strengthen their market positions. Competitive strategies include the development of advanced imaging technologies, expansion of portable device offerings, and partnerships aimed at improving clinical outcomes.

Companies covered in the market analysis include major multinational corporations and leading Japanese manufacturers. Detailed company analysis typically encompasses an overview of operations, key personnel, recent developments, revenue performance, and strategic initiatives. Continuous investment in research and development remains a critical factor for maintaining competitiveness in this evolving market.

Future Outlook of the Japan Ultrasound Device Market

The future of the Japan ultrasound device market appears positive, supported by demographic trends, technological progress, and evolving healthcare delivery models. Continued innovation in imaging quality, artificial intelligence integration, and device miniaturization is expected to enhance clinical utility and broaden adoption.

As Japan continues to address the healthcare needs of an aging population while promoting efficient and accessible care, ultrasound devices will remain central to diagnostic and therapeutic practices. Over the forecast period, the market is likely to witness steady expansion, with opportunities emerging in portable technologies, rural healthcare delivery, and advanced clinical applications.