Global Personal Computers Market Size, Share, Growth, and Forecast 2025–2033

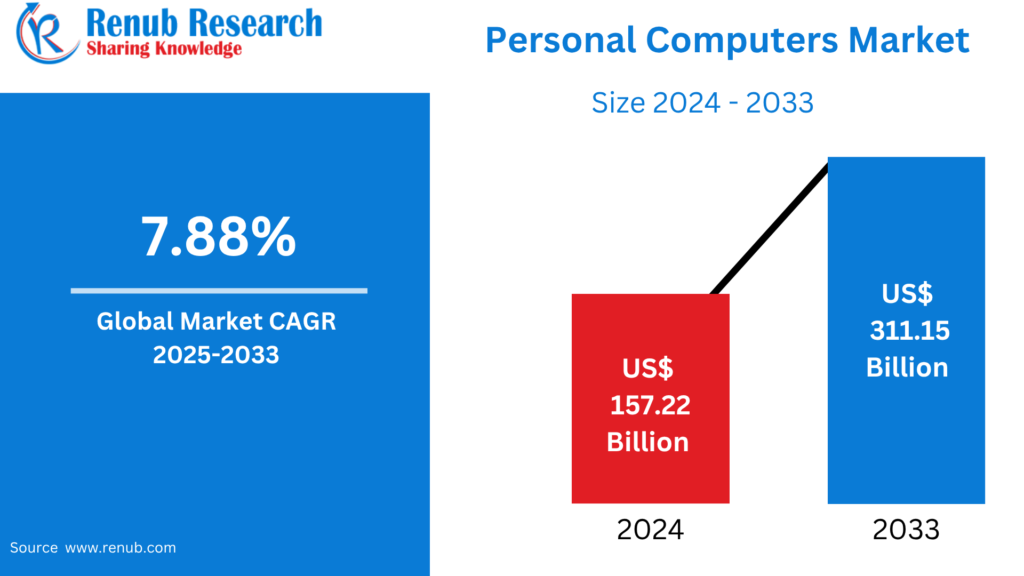

According to Renub Research Global Personal Computers Market is entering a strong growth phase as the world becomes increasingly digital, connected, and performance-driven. The market is projected to expand from US$ 157.22 billion in 2024 to US$ 311.15 billion by 2033, growing at a CAGR of 7.88% between 2025 and 2033. Rapid adoption of remote work systems, hybrid learning environments, gaming devices, and advanced computing technologies across households, enterprises, government institutions, and educational sectors are key factors shaping this remarkable growth trajectory.

Furthermore, technological innovation such as AI-enabled PCs, enhanced battery performance, ultra-slim designs, improved processors, and powerful graphic capabilities are redefining how personal computers are used globally. From professional workloads to entertainment, PCs continue to remain an essential digital foundation for individuals and organizations.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=personal-computers-market-p.php

Global Personal Computers Market Outlook and Industry Importance

Personal computers (PCs) play a crucial role in the modern digital ecosystem. Designed for individual use, they support activities ranging from browsing, communication, content creation, gaming, multimedia production, programming, and office productivity to advanced professional applications. A standard PC typically comprises a processor, RAM, storage, display, and operating system such as Windows, macOS, ChromeOS, or Linux.

PCs remain integral in homes, workplaces, educational institutions, healthcare facilities, government systems, creative studios, and business operations worldwide. With the expansion of digital services, online collaboration, and global connectivity, PCs have transitioned from luxury devices to necessary tools of daily life. Hybrid workforces, cloud computing adoption, and AI-powered features are further strengthening the importance of modern computers.

Demand remains strong across regions including North America, Europe, Asia Pacific, Latin America, and the Middle East. Countries like the United States, China, India, Japan, Germany, Brazil, and Saudi Arabia continue to lead both consumption and innovation trends.

Key Market Drivers Fueling the Global Personal Computers Market

Remote Work, Digital Learning, and Hybrid Operational Models

The pandemic fundamentally transformed global work and education structures. Even post-pandemic, remote and hybrid environments have remained relevant. Corporations now rely on personal computers for virtual meetings, cloud-based collaboration, cybersecurity operations, and enterprise computing systems. Educational institutions increasingly depend on laptops and tablets for e-learning platforms, virtual classrooms, and online examination systems. Innovation like AI-enabled PCs, enhanced security capabilities, and productivity upgrades are further stimulating adoption.

Rising Global Digitalization and Internet Access

Growing internet penetration across developing regions such as Asia Pacific, Latin America, and parts of Africa has fueled PC adoption at both consumer and enterprise levels. Internet users continue to grow worldwide, pushing demand for reliable computing devices to access digital platforms, e-commerce, banking, streaming services, telemedicine, online training, and communication networks. Governments and private sectors are also investing in digital infrastructure, boosting the need for PCs.

Growing Demand for Gaming, Content Creation, and High-Performance Computing

Gaming and content creation industries are witnessing massive global expansion. Professional gamers, streamers, video editors, animators, designers, and developers require advanced GPU and CPU-powered machines. Increasing popularity of esports, AI workloads, 3D rendering, and VR/AR experiences are further supporting performance-centric PC demand. Major brands are launching AI-powered gaming laptops, lightweight ultrabooks, and high-speed desktops to serve both professional and enthusiast markets.

Major Challenges in the Global Personal Computers Market

Supply Chain and Cost Challenges

The PC industry remains vulnerable to semiconductor shortages, geopolitical tensions, fluctuating raw material costs, logistics challenges, and component delays. Short supply of processors, memory chips, and display units can affect manufacturing timelines and pricing, particularly in cost-sensitive markets.

Market Saturation and Longer Device Lifecycles

Developed markets such as North America and Western Europe face maturity, with many consumers upgrading devices less frequently due to improved durability and software optimization. This extends replacement cycles and moderates unit shipments, prompting manufacturers to innovate aggressively to encourage replacements.

Segment-Level Insights of the Global Personal Computers Market

Laptops and Notebooks Market

Laptops dominate global PC demand because of portability, performance advancements, sleek designs, and battery efficiency. Ultrabooks, business laptops, gaming notebooks, and 2-in-1 convertibles appeal to students, professionals, travelers, and gamers alike. The shift toward mobile and flexible computing ensures strong long-term demand for notebook systems.

Consumer Personal Computers Market

Home users drive substantial demand for budget, mid-range, and entertainment PCs. Families use computers for streaming, online learning, browsing, social networking, and light productivity. Brands focus on design, affordability, user-friendly features, and bundled software to attract buyers.

Government and Education Personal Computers Market

Governments, public institutions, schools, and universities are among the largest PC procurers. They invest heavily in large-scale PC deployments to support digital governance, smart classrooms, research institutions, administrative tasks, and national digitization initiatives.

ARM-Based Personal Computers Market

ARM-based PCs are rapidly gaining popularity due to their extended battery life, efficient power usage, instant boot capabilities, thin structure, and improved performance. Enhanced software compatibility and rapid technological advancements are positioning ARM-powered systems as competitive alternatives to traditional architectures.

Mid-Range Personal Computers Market

Mid-range PCs remain the most popular choice worldwide as they balance performance and affordability. Suitable for professionals, students, and mainstream gamers, this segment provides efficiency, multitasking capability, and strong value for money.

Offline Retail and VARs Personal Computers Market

Although e-commerce continues to grow globally, offline retail stores and value-added resellers remain vital channels. These outlets provide physical demonstrations, customization support, after-sales assistance, financing plans, and trust — making them especially influential in emerging regions.

Windows Personal Computers Market

Windows PCs dominate worldwide shares due to vast application compatibility, enterprise preference, gaming ecosystem strength, and flexible system customization. Government institutions, enterprises, gaming users, and educational organizations rely heavily on Windows-powered systems.

Regional Market Highlights in the Global Personal Computers Market

United States Personal Computers Market

The U.S. represents one of the largest and most technologically advanced PC markets globally. Demand remains strong from enterprises, gamers, students, and hybrid workers. High purchasing power and innovation-friendly consumers support premium device adoption.

France Personal Computers Market

France maintains a stable and competitive PC market, supported by corporate digitalization, educational expansion, and strong consumer demand for laptops. Online and offline retail channels complement each other effectively.

India Personal Computers Market

India is among the fastest-growing PC markets worldwide. Increasing digital education, remote work adoption, government digitalization policies, and a rapidly expanding middle class significantly fuel market expansion.

Brazil Personal Computers Market

Brazil experiences rising demand from enterprises, consumers, and educational sectors despite economic constraints and import challenges. Local assembly initiatives and competitive pricing strategies strengthen availability.

Saudi Arabia Personal Computers Market

Saudi Arabia’s Vision 2030 digital transformation strategy drives massive investment in smart education, government modernization, and technological infrastructure, boosting strong PC adoption across government, education, and consumer sectors.

Market Segmentation of the Global Personal Computers Market

End User

Consumer

Small and Medium Business

Large Enterprise

Government and Education

Processor Architecture

x86 (Intel-AMD)

ARM-based

RISC-V & Others

Price Band

Entry-Level (< USD 600)

Mid-Range (USD 600–1200)

Premium / Gaming (> USD 1200)

Distribution Channel

Offline Retail and VARs

E-commerce and Direct-to-Consumer

Operating System

Windows

macOS

ChromeOS

Linux Distros

Competitive Landscape and Leading Companies in the Global Personal Computers Market

The global personal computers market is highly competitive, with leading technology giants continually innovating in design, speed, performance, AI integration, graphics, and energy efficiency. Strategic partnerships, new product launches, R&D investments, and regional expansion remain crucial growth strategies.

Major companies include:

Lenovo Group Limited

HP Inc.

Dell Technologies Inc.

Apple Inc.

Acer Incorporated

Microsoft Corporation

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Xiaomi Corporation

LG Electronics Inc.

Future Outlook of the Global Personal Computers Market

The future of the Global Personal Computers Market remains highly promising. Increasing digital transformation initiatives, AI-enabled computing systems, expanded gaming ecosystems, enhanced educational technology adoption, and enterprise modernization will continue fueling market growth. Continuous innovation in design, battery life, processing capability, cloud integration, and security will ensure that PCs remain central to global digital evolution between 2025 and 2033.