Reconstituted Milk Market Size and Forecast 2025–2033

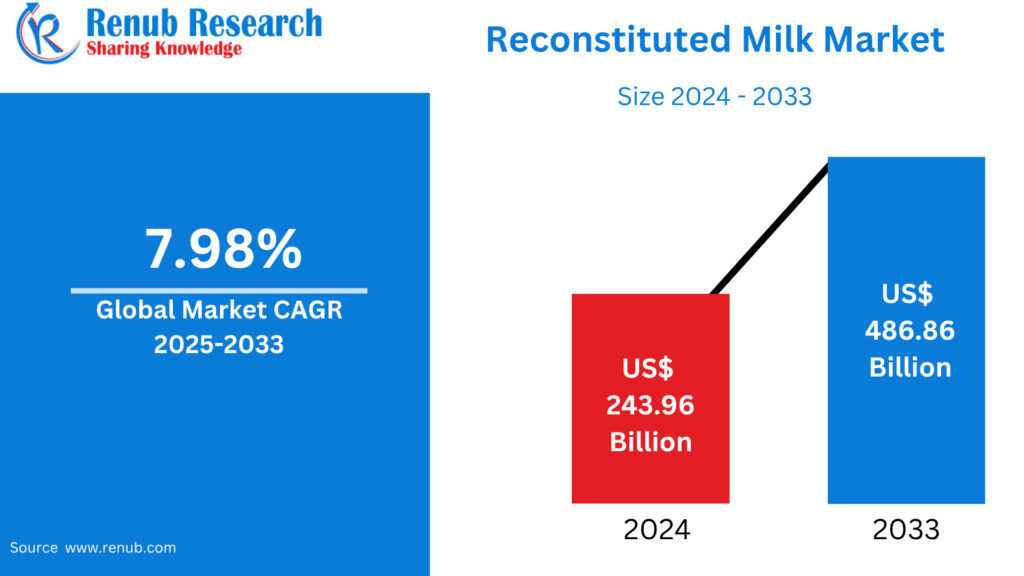

According To Renub Research global reconstituted milk market is poised for robust and sustained growth over the forecast period, driven by rising global dairy consumption, cost efficiency, and increasing demand for long-shelf-life food products. The market, valued at approximately US$ 243.96 billion in 2024, is expected to reach around US$ 486.86 billion by 2033, expanding at a compound annual growth rate of 7.98% from 2025 to 2033.

This strong growth trajectory reflects structural changes in global food systems, including urbanization, changing dietary habits, supply chain optimization, and the need to ensure consistent dairy availability in regions with limited fresh milk infrastructure. Reconstituted milk, produced by rehydrating milk powder with water, offers a scalable, affordable, and reliable alternative to fresh milk, making it a critical component of modern dairy supply chains worldwide.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=reconstituted-milk-market-p.php

Reconstituted Milk Industry Overview

The reconstituted milk industry encompasses the production, distribution, and consumption of milk obtained by adding water to milk powder, typically derived from whole or skimmed milk. This process allows milk to be produced in locations where fresh milk supply is inconsistent, expensive, or logistically challenging. Reconstituted milk is widely used across household consumption, food manufacturing, foodservice establishments, and institutional catering.

One of the primary advantages of reconstituted milk is its reduced dependency on cold-chain logistics. Milk powder can be stored for extended periods at ambient temperatures, significantly lowering transportation, storage, and spoilage costs. This makes reconstituted milk particularly valuable in developing economies, remote regions, and areas affected by seasonal milk shortages.

Urbanization and lifestyle changes have further accelerated demand for convenient and shelf-stable dairy products. Governments in several developing countries actively promote milk powder and reconstituted milk as part of food security and nutrition programs. In parallel, technological advancements in milk powder processing and rehydration techniques have improved taste, solubility, and nutritional retention, helping reconstituted milk compete more effectively with fresh milk in many markets.

Growth Drivers for the Reconstituted Milk Market

Rising Global Dairy Demand

The growing global demand for dairy products is one of the most significant drivers of the reconstituted milk market. Rising populations, increasing disposable incomes, and greater awareness of the nutritional benefits of dairy are boosting consumption of milk, cheese, yogurt, ice cream, and other dairy-based foods. This trend is particularly pronounced in emerging economies, where dietary patterns are shifting toward higher protein and calcium intake.

However, many regions face challenges in meeting dairy demand through fresh milk alone due to inadequate infrastructure, climatic limitations, and seasonal production variability. Reconstituted milk provides a practical solution by ensuring consistent supply and uniform quality regardless of geographic constraints. Its scalability and transport efficiency make it an essential tool for balancing global dairy supply and demand.

Extended Shelf Life and Reduced Waste

Extended shelf life is a key competitive advantage of reconstituted milk. Milk powder, the core raw material, can be stored for months without refrigeration, reducing spoilage and food waste. This feature is particularly valuable in regions with unreliable electricity, limited cold storage, or long transportation routes.

For manufacturers, retailers, and foodservice operators, longer shelf life enables bulk purchasing, better inventory management, and reduced operational losses. For consumers, it ensures product availability during emergencies, supply disruptions, or seasonal shortages. On a global scale, the shelf stability of reconstituted milk supports food security initiatives and facilitates international trade by allowing dairy products to be shipped over long distances without quality deterioration.

Technological Advancements in Processing and Rehydration

Technological progress has played a crucial role in improving the quality and acceptance of reconstituted milk. Advances in spray-drying techniques have resulted in finer milk powders with superior solubility and improved nutrient retention. Modern rehydration technologies allow milk powder to dissolve more evenly, delivering better texture, mouthfeel, and taste.

Packaging innovations have further enhanced product stability by protecting milk powder from moisture, contamination, and oxidation. Automation and digital monitoring in dairy processing facilities ensure consistent quality while reducing production costs. Additionally, fortification technologies enable manufacturers to enrich reconstituted milk with vitamins and minerals, making it attractive to health-conscious consumers and government nutrition programs. These innovations have significantly narrowed the perceived quality gap between reconstituted and fresh milk.

Challenges in the Reconstituted Milk Market

Supply Chain Dependency

The reconstituted milk market is highly dependent on a stable supply of milk powder, making it vulnerable to disruptions in the global dairy supply chain. Factors such as climate variability, disease outbreaks, trade restrictions, and geopolitical tensions can affect milk production and powder availability. Price volatility in raw milk and milk powder markets can also impact profitability and pricing stability.

Logistical challenges, including transportation delays and storage issues, can further disrupt supply, especially for cross-border shipments. To mitigate these risks, companies must diversify sourcing, invest in resilient logistics networks, and adopt strategic inventory management practices. However, these measures can increase operational complexity and costs.

Competition from Fresh Milk

Competition from fresh milk remains a significant challenge, particularly in regions with well-developed dairy infrastructure. Many consumers perceive fresh milk as superior in taste, texture, and nutritional value. In high-income and urban markets, reliable cold chains and strong local dairy branding reinforce consumer preference for fresh milk.

This perception can limit the adoption of reconstituted milk, especially among health-conscious consumers. Overcoming this challenge requires continuous improvements in product quality, transparent communication about nutritional equivalence, and targeted consumer education highlighting the safety, convenience, and reliability of reconstituted milk.

United States Reconstituted Milk Market

The reconstituted milk market in the United States is experiencing steady growth, driven by demand for affordable, convenient, and nutritionally enhanced dairy products. Consumers are increasingly interested in fortified, high-protein, and flavored milk options that align with active lifestyles and wellness trends. Single-serve and environmentally friendly packaging formats are also gaining traction among busy urban consumers.

Despite these opportunities, challenges remain related to consumer perceptions of taste and nutritional quality compared to fresh milk. Supply chain dependence on milk powder and environmental concerns associated with dairy production also influence market dynamics. Nevertheless, ongoing product innovation and sustainability initiatives are expected to support continued growth in the U.S. market.

Germany Reconstituted Milk Market

Germany’s reconstituted milk market is growing steadily, supported by demand for cost-effective and convenient dairy solutions. Health-conscious consumers are driving interest in fortified and protein-rich milk products, while younger demographics favor flavored varieties and sustainable packaging.

However, the market faces challenges related to consumer preference for fresh milk and concerns about environmental impact. Dependence on consistent milk powder supply also poses risks. Continued innovation, alignment with sustainability goals, and transparent communication about product quality are expected to help the market maintain its growth trajectory.

India Reconstituted Milk Market

India represents one of the fastest-growing markets for reconstituted milk due to rapid urbanization, rising dairy consumption, and the need for affordable, shelf-stable products. Reconstituted milk plays a critical role in addressing supply-demand gaps caused by seasonal fluctuations and infrastructure limitations.

Single-serve sachets and small packaging formats cater to urban lifestyles and price-sensitive consumers. Increased health awareness is driving demand for fortified and high-protein variants. Expanding distribution networks, particularly in rural and semi-urban areas, are further supporting market growth. Together, these factors position India as a key growth engine for the global reconstituted milk market.

Saudi Arabia Reconstituted Milk Market

The reconstituted milk market in Saudi Arabia is expanding steadily due to urbanization, changing lifestyles, and increasing demand for convenient food products. Milk powder is widely used because of its long shelf life and versatility in cooking and beverage preparation.

Consumer preferences are also shifting toward healthier and specialized dairy options, including fortified, lactose-free, and premium formulations. These trends align with broader regional movements toward balanced nutrition and wellness. Manufacturers are responding by diversifying product portfolios to meet evolving consumer expectations, supporting sustained market growth in the country.

Recent Developments in the Reconstituted Milk Market

Regulatory authorities in several countries have intensified efforts to ensure the safety and quality of milk products, including reconstituted milk, reflecting growing consumer awareness and demand for transparency. Investments in large-scale dairy processing facilities highlight the industry’s focus on improving efficiency, capacity, and product consistency.

Such developments demonstrate the sector’s commitment to modernization, regulatory compliance, and long-term sustainability. Continued investment in processing infrastructure and quality assurance is expected to strengthen market confidence and support global expansion.

Reconstituted Milk Market Segmentation

By Type

The market is segmented into skimmed milk, whole milk, anhydrous milk fat, and unsalted frozen butter. Skimmed and whole milk powders dominate due to their widespread use in household consumption and food manufacturing. Anhydrous milk fat and unsalted frozen butter are primarily used in industrial and specialty applications.

By Application

Applications include milk, cheese, yogurt, ice cream, and others. Liquid milk applications account for a significant share, while cheese, yogurt, and ice cream manufacturing increasingly rely on reconstituted milk for consistency and cost control.

By Distribution Channel

Distribution channels are divided into business-to-business and business-to-consumer segments. The B2B segment serves food manufacturers, bakeries, and foodservice operators, while the B2C segment includes online sales, hypermarkets and supermarkets, wholesale stores, and other retail formats. Growth in e-commerce is improving consumer access and convenience.

Conclusion

The global reconstituted milk market is set for strong and sustained growth through 2033, driven by rising dairy demand, shelf-life advantages, cost efficiency, and technological progress. While challenges such as supply chain dependency and competition from fresh milk persist, ongoing innovation, government support, and expanding applications across foodservice and manufacturing are expected to offset these constraints.

As global food systems continue to prioritize affordability, availability, and sustainability, reconstituted milk will remain a vital component of the dairy industry, supporting nutrition, food security, and economic efficiency across diverse markets worldwide.