Many taxpayers file income tax returns every year without fully understanding two basic terms that appear in every tax form: financial year and assessment year. While they sound similar, they serve different purposes in the tax system. Confusion between the two can lead to incorrect filing, wrong tax calculations, and mistakes in reporting income.

Understanding the difference between assessment year and financial year becomes even more important when you have multiple income sources such as salary, interest, capital gains, or business income. It is also relevant for investors, because certain investment products have restrictions such as a lock in period, which determines when you can redeem or claim benefits.

This article explains why financial year and assessment year matter, and how they affect tax compliance.

What is a financial year?

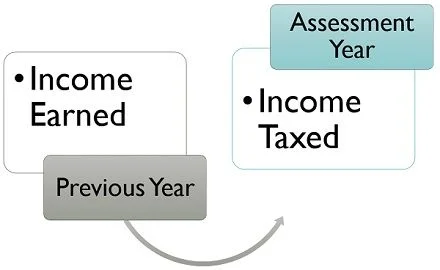

A financial year is the 12-month period during which you earn income. In India, the financial year runs from 1 April to 31 March.

For example, if you earn salary, interest, or investment gains between 1 April 2025 and 31 March 2026, that income belongs to the financial year 2025–26.

All income earned during the financial year must be reported in the income tax return.

What is an assessment year?

An assessment year is the year in which the income earned in the financial year is assessed and taxed. The assessment year immediately follows the financial year.

Using the same example:

- Financial year: 2025–26

- Assessment year: 2026–27

This means income earned between April 2025 and March 2026 is assessed and taxed in the period April 2026 to March 2027.

This is why income tax return forms and notices always refer to the assessment year.

Why the difference matters for filing

The difference between assessment year and financial year matters because your income tax return is always filed for the assessment year, even though the income belongs to the financial year.

Many taxpayers accidentally select the wrong year while filing returns online. This can cause:

- incorrect reporting of income

- mismatch with Form 16 or Form 26AS

- delays in processing refunds

- potential notices for discrepancies

Understanding the assessment year and financial year relationship helps avoid these errors.

How it affects Form 16, AIS, and Form 26AS

Tax documents are aligned to financial years, but reporting and filing happens in the assessment year.

For salaried taxpayers:

- Form 16 is issued for the financial year

- TDS credits reflect the same financial year

- The income tax return is filed in the following assessment year

AIS and Form 26AS also display transactions in financial-year format. If you misinterpret the year, you may end up missing income entries or reporting them in the wrong return.

Why it matters for investment reporting

For investors, the financial year determines when a gain or loss is counted.

For example:

- If you sell mutual fund units in March, the capital gain belongs to that financial year.

- If you sell in April, it belongs to the next financial year.

This timing affects tax filing and reporting.

It also matters for products that come with restrictions such as a lock in period. A lock-in period determines when you can redeem the investment, but the tax impact depends on the financial year in which redemption occurs.

Understanding lock-in period and its tax relevance

A lock-in period means you cannot redeem or withdraw money before a specified duration. Some investment products are designed this way to encourage long-term savings or ensure stability.

For example, certain tax-saving mutual fund schemes and other instruments have a lock-in period. Even if the lock-in ends, the tax event happens only when you redeem or withdraw.

This is where assessment year and financial year become relevant again. The redemption date decides the financial year in which the gain is taxed, and the return is filed in the following assessment year.

Impact on deductions and tax benefits

Many deductions are allowed based on investments made during the financial year. If you invest after 31 March, the benefit is not available for that financial year.

For example, if you invest in eligible tax-saving instruments on 2 April, the deduction will apply to the next financial year, not the one that just ended.

This is why tax planning deadlines usually focus on 31 March, which marks the end of the financial year.

How it affects refunds and processing

Refunds are processed in the assessment year, because the return is filed in that year. If you delay filing, refund processing also gets delayed.

Additionally, if you file for the wrong assessment year, your return may be treated as defective or invalid, leading to further complications.

Common mistakes taxpayers make

Some frequent mistakes include:

- confusing the financial year with the assessment year while filing

- selecting the wrong year on the tax portal

- reporting income from the wrong period

- missing investment transactions due to year confusion

- assuming lock-in completion automatically creates a tax event

These errors are avoidable once you clearly understand the two-year structure.

Conclusion

The difference between assessment year and financial year is one of the most basic but important concepts in income tax filing. The financial year is when you earn income, while the assessment year is when that income is taxed and the return is filed. Confusing the two can lead to incorrect filing, mismatches in TDS credits, and delays in refunds.

This understanding is especially important for investors, where timing of redemption and factors such as a lock in period can affect which financial year the income belongs to. Once you understand the structure, filing becomes more accurate and far less stressful.